Why Tempus AI Looks Different in 2026

Fundamental analysis of $TEM

A quick note before we start: My last deep dive on Tempus was a bit too technical. This version is written to be easier to follow if you do not work in healthcare or biotech every day along with some 2026 updates.

Healthcare has a structural problem with math. The United States spends more than 4.5 trillion dollars annually, yet most clinical decisions are still made with fragmented information. The genomic report is in one system. Imaging is in another. The pathology slide is a PDF. Outcomes data, if it exists, rarely makes it back to the doctor who ordered the test.

Tempus was founded in 2015 to fix that fragmentation. The idea was straightforward: connect clinical, molecular, imaging, and outcomes data at scale so medicine can move from retrospective averages to individualized predictions. In 2026, that idea has become an operating business.

From Narrative to Operating Results

For years, Tempus was labeled a healthcare AI story. The market priced it as a diagnostics company with a data project attached. 2025 was the year the financials began to validate the platform thesis. Revenue inflected. Margins expanded. The company reported its first quarter of positive adjusted EBITDA. The FDA cleared additional AI tools for clinical use.

What was once conceptual is now part of daily practice. Oncologists use Tempus reports to guide therapy. Pharma companies use the platform to design trials and find patients. Health systems build Tempus alerts into care pathways.

Management Q&A Highlights: What Eric Lefkofsky Said in 2026

These are the three exchanges from 2026 that best explain how management sees the business right now.

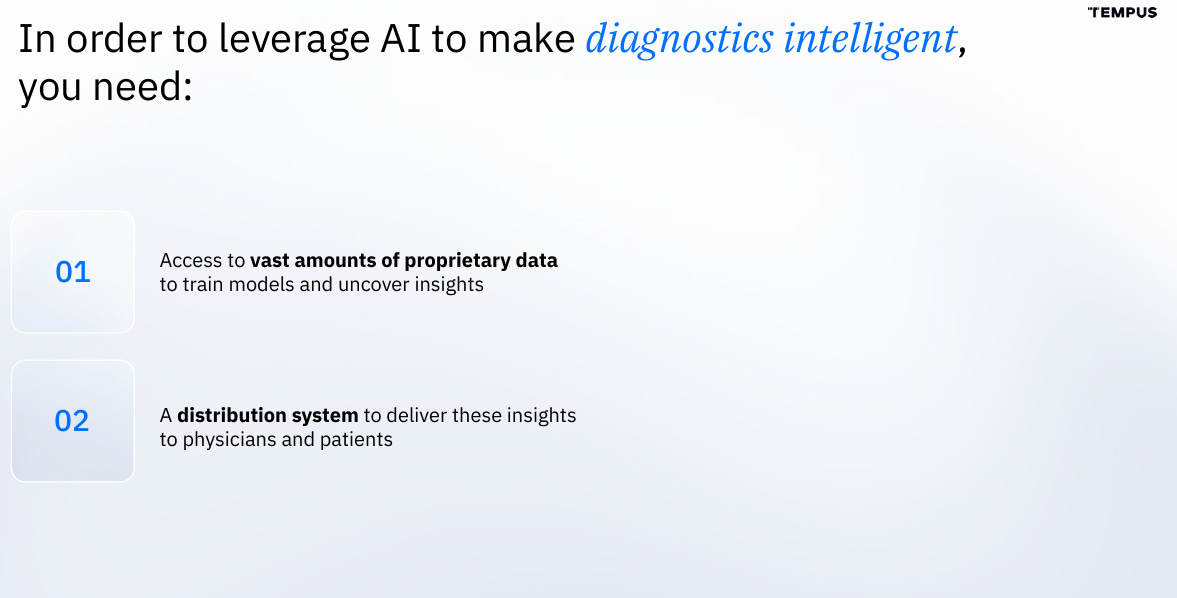

1. On why Tempus is not just a lab

J.P. Morgan Healthcare Conference, January 12 2026

Question: You have spent 10 years building Tempus. What was the original problem you were solving?

Eric Lefkofsky: “10 years ago, we started Tempus to solve a single problem, could AI enabled diagnostics unlock precision medicine. In order to do so, you really need two things. You need access to vast amounts of proprietary data to train models and uncover insights and you need a distribution system to deliver those insights to the hands of physicians and patients.”

My take: Lefkofsky still frames diagnostics as the vehicle, not the destination. The labs in Chicago, Atlanta, RTP, and the Ambry facility are the distribution system. The asset is the data used to train models. That is why he invested in Ambry and Paige even when they pressured near term margins. He is telling investors to value the platform, not the test volume.

2. On the Data and Insights business scaling

Q1 2026 Earnings Call, May 5 2026

Question: Can you break down the strength in Data and Applications this quarter?

Eric Lefkofsky: “Our data and applications business did extraordinarily well. 87 million dollars of revenue representing 40.5 percent year over year growth, with particular strength in our data licensing and modeling business insights, which grew over 44 percent. This is our third straight quarter of bookings north of 100 million dollars.”

My take: This is the first time management has led with the data segment on an earnings call. Diagnostics grew 35 percent, but Lefkofsky highlighted the 44 percent growth in data licensing. Bookings over 100 million dollars for three quarters signals that pharma is committing multiyear dollars. That mix shift is what moved gross margins into the high 60s and turned adjusted EBITDA positive. He is guiding the market to re rate Tempus on platform economics, not lab multiples.

3. On the Ambry integration and why germline matters

Goldman Sachs Healthcare Conference, June 8 2026

Question: How does Ambry fit into the Tempus model, and why buy a hereditary testing business?

Eric Lefkofsky: “We didn’t set out to just be a lab. We set out to solve a problem, which was how do you contextualize these sequencing results in a way that would allow you to figure out what’s the right path for this patient. And so to do that, we needed clinical data. Ambry added one of the deepest hereditary cancer and cardiology variant databases in the market. When you combine inherited risk with somatic tumor data and outcomes, you can start to predict not just therapy response, but who should be screened, who is at risk, and how you manage patients across their lifetime.”

My take: Ambry was not a revenue tuck in. It expanded Tempus from oncology treatment into prevention and risk. In May 2026, Tempus finished integrating Ambry’s germline database into Lens. Pharma can now query inherited and somatic variants together. That is a capability no other commercial platform has. It also explains the Roche deal. Partners are paying for multimodal data that links prevention, diagnosis, and treatment.

What the Platform Actually Does Today

Tempus operates at the intersection of four data types that historically did not communicate:

Next generation sequencing from tumor tissue and blood

Whole slide digital pathology images

Structured and unstructured electronic health record data

Longitudinal outcomes, including treatment response, recurrence, and survival

The key is that Tempus trains models across all four at once. A genomic alteration by itself may not be informative. That same alteration, viewed with pathology morphology, prior therapy, and real world outcomes, becomes actionable. That multimodal approach is difficult for traditional labs or single purpose AI companies to replicate.

Those models are then deployed back into workflows. Physicians receive reports that highlight therapy options, clinical trial matches, and risk stratification, not just a list of variants. Pharma partners can identify eligible cohorts for Phase 2 studies in days. Hospitals receive care pathway prompts when patients meet specific criteria.

Every interaction creates new data. New data retrains the system. The system improves. That feedback loop is the core of the business.

Tempus Has Physical Infrastructure Too

This is not just a software company. Tempus operates CAP accredited and CLIA certified laboratories in Chicago, Atlanta, and Research Triangle Park. These facilities run the xT, xF, xR, and MRD tests that generate the data layer.

The lab footprint expanded materially with the 2024 acquisition of Ambry Genetics. Ambry brought a dedicated sequencing facility in North Carolina, a large germline testing business, and one of the most comprehensive hereditary cancer and cardiology variant databases in the market. The Ambry lab continues to operate and is now fully integrated into the Tempus network. That gives the company a West Coast presence for faster turnaround and adds inherited risk and rare disease to the platform.

Physical labs matter for two reasons. First, you cannot build multimodal AI without controlling the wet lab that generates clean, consistent data. Second, reimbursement and regulation require CLIA and CAP standards. Owning the lab means Tempus controls quality, turnaround time, and cost structure as it scales.

2025 Drove the Re rating, 2026 Is Adding to It

The 2025 results showed the flywheel is working. Full year revenue was approximately 1.265 billion dollars, up about 80 percent year over year. Q3 revenue was 334.2 million dollars, with genomics up 117 percent year over year. The revenue mix is shifting. Data and Insights, the high margin pharma licensing business, is accelerating and moving non GAAP gross margins into the mid to high 60 percent range.

Adjusted EBITDA turned positive in Q3 2025 at 1.5 million dollars. Full year guidance remained slightly positive despite a 20 million dollar integration cost from the Paige acquisition. GAAP profitability is still a 2027 to 2028 goal but I believe the structure is there to accomplish it.

The data asset also expanded. Tempus holds more than 400 petabytes of de identified multimodal data, 40 million research records, and longitudinal coverage of over 60 percent of United States oncology patients. The Paige acquisition added 7 million digitized pathology slides and FDA cleared computer vision.

What’s New in 2026

The first half of 2026 has added several updates that strengthen the thesis:

Q1 2026 performance: Preliminary results in April showed Q1 revenue above 360 million dollars. Data and Insights reached 22 percent of total revenue, up from 19 percent in Q4 2025. Adjusted EBITDA was positive for the second straight quarter. Management raised full year 2026 guidance to 1.55 to 1.60 billion dollars, implying 23 percent to 27 percent growth.

Medicare MRD coverage: In February 2026, CMS expanded Medicare coverage for minimal residual disease testing in solid tumors. Tempus received positive local coverage determinations in three additional regions. This reduces a major reimbursement overhang for the diagnostics business and should support test volume growth through 2027.

Radiology entry: In March 2026, Tempus received FDA 510(k) clearance for Lung nDetect, an AI tool that helps radiologists quantify lung nodule progression on CT. This is the company’s first clearance in radiology and adds a third clinical domain alongside oncology and cardiology.

Ambry data integration: In May 2026, Tempus completed the technical integration of Ambry’s germline database into Lens. Pharma partners can now query inherited and somatic variants together when designing trials. The combined dataset exceeds 8 million clinical and molecular records with family history linkage.

New pharma agreement: Tempus signed a multiyear partnership with Roche in January 2026 to co develop data and models for early oncology assets. The deal includes upfront payments and milestones. Total committed contract value across the top 20 pharma partners is now above 900 million dollars.

International buildout: Non United States revenue grew 58 percent year over year in Q1 2026. Tempus opened a London hub in March to support EU data partnerships and is pursuing CE marking for its cardiology ECG tools, with launch targeted for late 2026. The company also signed its first hospital network deal in Japan in May 2026 to begin digitizing pathology slides for research use.

How Tempus Makes Money

Genomics and diagnostics were about 78 percent of Q1 2026 revenue. The portfolio includes xT for tumor profiling, xF for liquid biopsy, xR for RNA, MRD for recurrence monitoring, and Ambry’s hereditary cancer and cardiology panels. Annual test volume is now above 550,000 across the combined lab network. Reimbursement is improving, EHR integrations are deeper, and lab automation across Chicago, Atlanta, RTP, and the Ambry facility is driving leverage. The internal goal of a 1 billion dollar diagnostics run rate by 2028 still looks achievable.

Data and Insights is 22 percent of revenue and growing. This segment licenses de identified real world data and AI models to pharma for target discovery, trial design, and regulatory submissions. Contracts are multiyear, switching costs are high, and incremental margins look like software. Over time, this business should drive most of the company’s cash flow.

Why the Application Layer Matters

Revenue tells you how Tempus gets paid. Applications explain why it is hard to replace.

At the point of care, Tempus is shifting from descriptive to predictive. Instead of listing mutations, the report says, based on 80,000 similar patients, the response rate to this therapy was 34 percent. In oncology, tumor, liquid, RNA, MRD, and germline data from Ambry are used together to detect recurrence earlier and adjust treatment.

For pharma, the most immediate value is trial matching. Tempus screens its network in real time to find patients who meet complex criteria. The same system supports biomarker validation and companion diagnostic development. The time savings are material, which is why AstraZeneca, GSK, and now Roche have signed nine figure deals.

Pathology became foundational after the Paige acquisition in 2025. Because most cancer diagnoses start with a slide, owning that step strengthens every downstream model. Cardiology was the first step outside oncology, with FDA cleared ECG algorithms for atrial fibrillation and low ejection fraction. Radiology is now the third domain after the Lung nDetect clearance in March.

International revenue is scaling through pharma data deals. The business is capital light and margin accretive. Regulation is the main constraint, but the London hub and CE mark work are addressing it.

Each application generates more data. More data improves the models. Better models win more applications. That is how a platform compounds.

Why This Is Hard to Replicate

Three structural advantages matter in 2026.

First, the data. Forty million longitudinal patient records with paired genomics, imaging, clinical notes, and outcomes cannot be built quickly. Ambry Genetics added a germline database and hereditary testing workflows that would take years to reconstruct. Paige added millions of pathology slides.

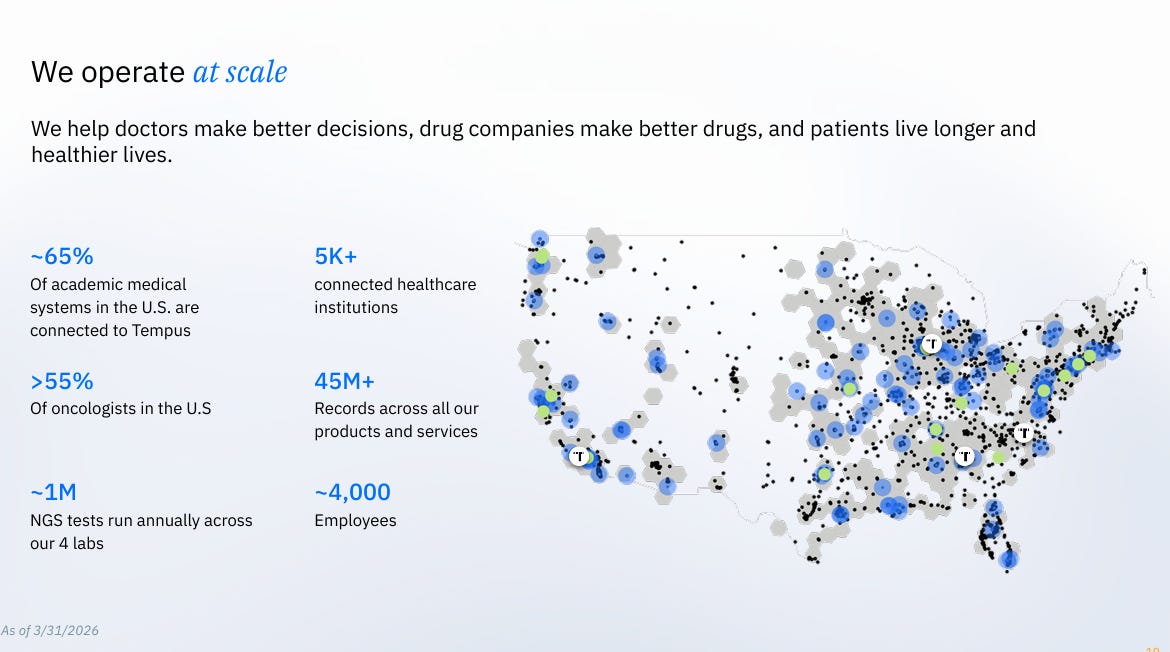

Second, workflow integration. Tempus is embedded in more than 4,500 hospital systems. Physicians order and review tests in Tempus Hub. Researchers build cohorts in Lens. Care teams receive prompts from Next. Once software is part of daily clinical practice, switching is expensive.

Third, network effects. Every new test improves the models. Improved models increase clinical utility. Higher utility drives adoption. Adoption generates more tests. The top 20 pharma companies are funding and deploying the cycle, which accelerates the flywheel.

Risks That Still Matter

The bear case in 2026 is about execution and timing, not the underlying idea.

Reimbursement still controls the diagnostics business. The recent CMS MRD expansion helps, but payor decisions can still slow growth before Data and Insights is large enough to offset it.

Pharma revenue is lumpy by nature. Contracts are large and renewal timing varies. A delayed renewal can impact a quarter even if the multiyear trend is intact.

Expansion beyond oncology carries operational risk. Cardiology and radiology require separate regulatory and commercial work. If they consume capital without generating meaningful revenue by 2027, the market may revalue Tempus as an oncology only company.

Dilution remains the quiet risk. The company refinanced into 750 million dollars of 0.75 percent convertible notes due 2030, with a 84.19 dollar conversion price. That reduced interest expense and extended maturity. But leverage is still high relative to equity and free cash flow is not yet positive. If the share price rises, dilution occurs. If growth slows and cash burn continues, future financing could be dilutive.

A bear scenario for 2026 to 2027 looks like this. Diagnostics growth slows to the mid teens. Data and Insights has a renewal gap. New verticals take longer to monetize. Investor patience thins. The multiple compresses, share count rises, and returns lag the quality of the business.

Why the Thesis Holds in 2026

I am not going to pretend like there aren’t risks but these are largely timing and execution related. The data has been aggregated. The lab network across Chicago, Atlanta, RTP, and the Ambry facility is scaled. The integrations into 4,500 hospitals are live. The regulatory clearances are in hand for oncology, cardiology, and now radiology. Operating leverage appeared in 2025 and continued into Q1 2026.

What Tempus Is Actually Worth in 2026

Tempus is hard to value with the usual shortcuts. At 6-7 times TTM sales (as of 6/11/2026), the market is treating it like a diagnostics lab with a little AI sprinkled on top. That price gives you the genomics business and basically assumes the data platform is worth nothing.

Here’s a base case that I think is pretty conservative.

1. Growth: Start with 25 percent revenue growth off the 2026 guidance of around 1.575 billion dollars. That is already slower than the 36 percent Tempus just posted in Q1 and way below the 80 percent growth we saw in 2025. It assumes diagnostics settles into the mid teens and Data and Insights grows around 30 percent, not the 44 percent we saw last quarter. So we are modeling a slowdown everywhere.

2. Margins: Assume the business eventually gets to 15 percent free cash flow margins. Non GAAP gross margins are already in the high 60s because Data and Insights is high margin and it keeps taking share. That segment was 22 percent of revenue in Q1 and growing fast. If it becomes 35 percent of the mix in a few years, 15 percent free cash flow is not heroic. It actually assumes the lab business stays pretty low margin even with all the automation we are seeing in Chicago, Atlanta, RTP, and the Ambry facility.

3. Discount rate: Use 10 percent. That covers dilution, reimbursement risk, and the fact that Tempus is still pushing into cardiology and radiology. The company refinanced into 750 million dollars of converts due 2030 with a 84.19 dollar strike. If the stock never gets there, dilution is limited. If it does, you are probably happy. Either way, 10 percent feels fair for a business that is not GAAP profitable yet.

Run that math and you get intrinsic value near 95 dollars per share. That is a 10 year DCF with 4 percent terminal growth.

Why I call this conservative:

First, we are going easy on Data and Insights. We modeled 30 percent growth when it just did 44 percent, and we already have three quarters in a row of bookings above 100 million dollars. Total committed contract value from the top 20 pharma partners is over 900 million dollars after the Roche deal. If that segment actually compounds at 35 to 40 percent, the math pushes intrinsic value well above 120 dollars without changing anything in diagnostics.

Second, we give diagnostics no credit for operating leverage. MRD just got broader Medicare coverage. Ambry is integrated. Lab automation is improving. We assume margins stay thin anyway.

Third, we assign zero value to the new stuff. Radiology got FDA cleared in March with Lung nDetect. Cardiology has already run over 1 million ECGs through the platform. International grew 58 percent last quarter. None of that is in the model.

So what are you paying for currently? You are buying a diagnostics business growing mid 20s that should hit a 1 billion dollar run rate by 2028. The data platform comes for free. That includes Ambry’s germline database, 7 million Paige pathology slides, the Roche and AstraZeneca deals, and all the optionality in radiology and international.

If Data and Insights keeps scaling and the market starts valuing it like a healthcare data company instead of a lab, the stock re rates. If it does not, you still own a real diagnostics business at 6-10 times sales with a founder who has been executing for 10 years.

The difference between 50 and 95 is really a bet on whether the flywheel compounds faster than dilution and skepticism. After Q1 2026, that bet feels a lot more reasonable than it did last year.

How to Think About It

Tempus is infrastructure for precision medicine. Infrastructure does not re rate in a straight line. There will be quarters where reimbursement is soft or a pharma contract slips. There will be headlines about competition or regulation. If you need a clean narrative every 90 days, this will be frustrating.

Taking a multiyear view, the direction in 2026 is clearer than it was in 2024. Tempus took a decade old data problem, built the infrastructure to solve it, and is now running significant volume through it. Physicians use it. Pharma pays for it. Regulators have cleared it. The financials are beginning to show it.

This is a long duration position. Size it for volatility. Dollar cost averaging makes more sense than trying to time an entry. The path to GAAP profitability will have uneven quarters.

The healthcare system will not solve its data problem on its own. It needs a backbone that connects information to decisions at the point of care. As of 2026, Tempus is the most advanced version of that backbone in the market.

This is not financial advice. Conduct your own diligence. Healthcare, artificial intelligence, and reimbursement are all subject to rapid change, and execution risk remains material.

Great analysis - concise and comprehensive. The long-term platform thesis, current trajectory, present reality, and a grounded bearish scenario for Tempus AI.